The U.S. airline industry emerged battered from a third quarter that was bookended by a global IT outage and two major hurricanes.

Nevertheless, optimism abounds in post-election sentiments that anticipate higher consumer demand, lower oil prices, and cuts to corporate taxes.

In May, we published a paper cautioning that the U.S. airline industry was about to see its pilot hiring bubble pop. Our hypothesis, we argued, would be confirmed if hiring pauses, furloughs, and layoffs were followed by cancellations, reductions, or deferments in aircraft orders.

The ensuing six months have only bolstered our confidence in this prediction.

On Nov. 18, Spirit announced that it had filed for Chapter 11 bankruptcy. The ultra-low-cost carrier previously stated its intention to furlough over 500 pilots and to defer all aircraft scheduled to be delivered from 2025-2026 for five years. These moves preceded Spirit’s plans to sell 23 Airbus jets from its fleet and to cut $80 million in costs in 2025 — savings that would be driven primarily by workforce reductions.

South for Southwest?

Spirit is not alone in struggling, however.

Attempting to establish a ceasefire with activist investment firm Elliot Management, Southwest recently unveiled its three-year transformation plan at its Investor Day event. While many of the headlines were devoted to this plan’s flashy changes to the airline’s open seating model, there was plenty of red meat under the hood.

Southwest is seeking to bring its capacity in balance with passenger demand. To increase utilization (and thus reduce unit costs), the carrier is rolling out redeye flights for the first time in its 58-year history. The airline is also aiming for a five-minute reduction in its already-low turn times.

The moves most relevant to our thesis, however, come from Southwest’s plans to trim its workforce and to tighten its capital expenditures on aircraft from $2.1 billion per year to $0.5 billion. Southwest had hoped to let its workforce shrink naturally via attrition, targeting a reduction of 2,000 employees in the final quarter of 2024.

Evidently, the carrier was not on track to hit this target, as it announced a “Voluntary Separation Program” in mid-November. This program, eligibility for which extends to agents in customer service, cargo handling, provisioning, and more, hopes to alleviate overstaffing at 18 airports. Crucially, this program does not yet extend to pilots.

Yet the Dallas-based airline is curtailing its presence at Atlanta Hartsfield Jackson International Airport, aiming to cut 140 pilots by April 2025. While it is expected that Southwest will offer the affected employees relocation to one of its other bases, not all pilots are guaranteed their desired location, which might cause further attrition.

Passengers Fill Seats, Not Coffers

Even though 2024 has been one of the busiest years on record for passenger travel, airlines across the industry continue to struggle with numbers that are not in their favor.

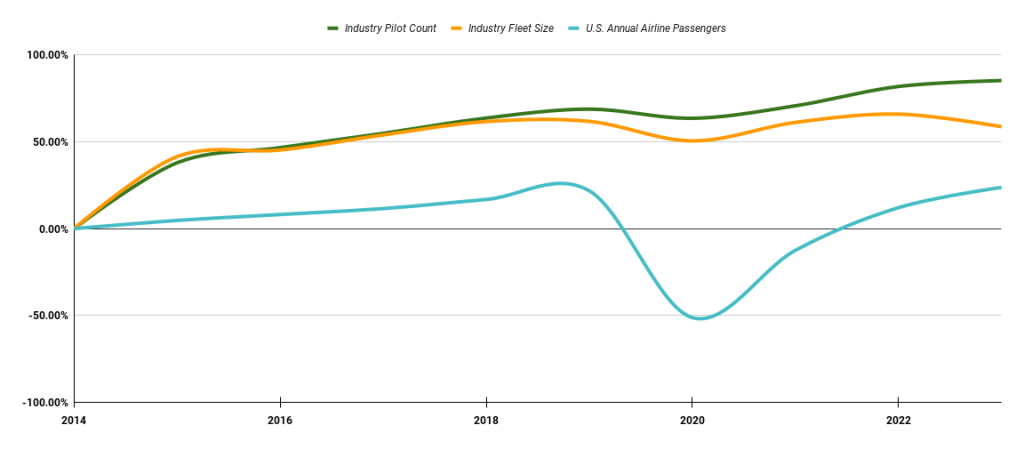

Between 2014 and 2023, the number of pilots relative to a carrier’s total number of aircraft rose at a compound annual growth rate of 7.08%. Over the same period, fleet size grew 5.26% and passenger volume ticked up only 2.39%.

To be fair, the fact that airlines’ growth in fleet sizes has slowed in recent years is not entirely under their control. The beleaguered aircraft manufacturer Boeing has made a string of errors (many of which were unforced) of late. For example, after resolving a seven-week strike with its machinists’ union, Boeing announced in mid-November that it would lay off more than 2,500 U.S. workers before Christmas, part of its larger plan to trim its global workforce by 10%, or 17,000 positions.

While Spirit’s deferments open up slots for other airlines to receive deliveries faster from Airbus, not all airlines are positioned to take advantage of this opportunity. Southwest famously runs an all-Boeing fleet and has repeatedly denied that Boeing’s troubles will force the carrier to consider adding Airbus jets.

Still, it cannot be denied that Boeing’s inability to meet its deadlines provides a highly convenient scapegoat for an airline that wishes to slow its hiring growth without also spooking its investors.

If airlines expect continued growth in passenger volumes, a higher pilot-to-aircraft ratio might be justified — provided also that the margins support this decision. But the margins for flying passengers around are simply not worth it, with the profit for many carriers coming from alternative streams of revenue.

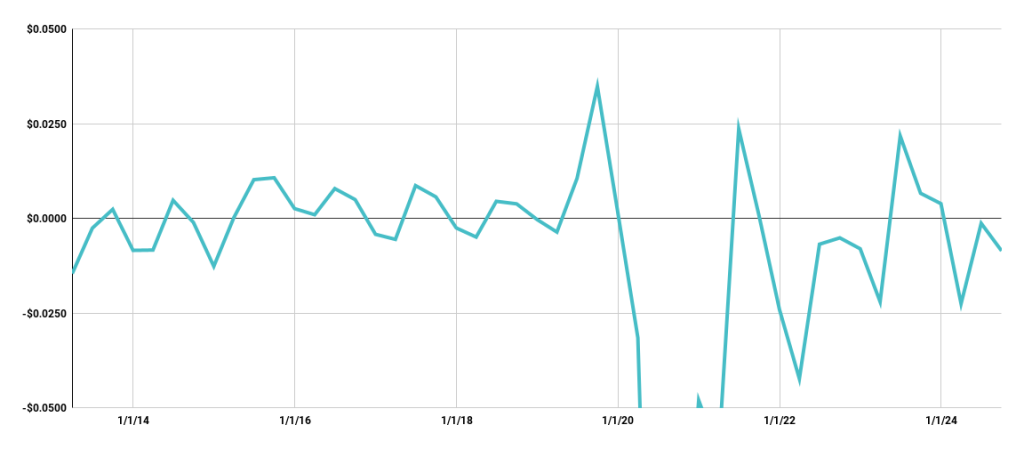

By subtracting the passenger revenue per available seat mile (or PRASM) from an airline’s cost per ASM (CASM), we can deduce the passenger margin per ASM: the inelegantly titled PMASM. Studying PMASM allows us to track an airline’s operational efficiency relative to demand.

In even the best of times, airlines are generating margins from passenger revenue alone worth only pennies per ASM. Of course, once airlines begin to provide billions of ASMs in a given quarter, these pennies quickly add up.

But such margins are found in the best of times. In the first three quarters of 2024, the industry’s average PMASM (weighted by airlines’ ASMs) has been negative.

Q3 saw only two carriers post a positive PMASM: United and Alaska. The remaining carriers — except JetBlue, Hawaiian, and Allegiant — reported positive overall margins per ASM on the strength of their loyalty rewards programs and other revenue line items.

The goal for airlines now is to break even with passenger revenues and compensate with profits made elsewhere. But the cyclical nature of passenger travel, doubled by its sensitivity to overall economic conditions, makes it difficult to generate positive or even breakeven passenger margins on a regular basis.

So, in order to keep PMASM at least as close to zero as possible, airlines are forced to carry out cost-saving measures — such as implementing slowdowns in pilot hiring.

Cloudy With a Chance of Sun

Even though newly trained pilots are facing an uphill battle in the coming years, the forecast is not uniformly dismal.

Data from the Future & Active Pilots Advisors (FAPA) shows that pilot hiring growth in the year-to-date is up 13% over 2019.

On the other hand, FAPA data also portrays the struggle of certain airlines — neither American Airlines nor JetBlue have hired a single pilot from June to October. Certain carriers that are heavily reliant on Boeing have posted several months in 2024 where no pilots were hired, such as Southwest’s five (compared to one in 2019) and United’s two (compared to none in 2019).

Regardless, industry leaders are optimistic that 2025 will be a return to form in hiring. Delta, which has so far seen its hiring growth slow 50% on a yearly basis, predicts that the industry will see a “more normalized” tempo next year.

Delta President Glen Hauerstein voiced an especially bullish outlook for 2025, as he forecast that U.S. airlines will hire roughly 5,000 new pilots next year — a feat missed in 2019 by only 23 hires.

For the best insights on the pilot workforce, go to FindAPilot.com, where you can search hundreds of pilot jobs and tens of thousands of pilots for hire.